Do Your Best From The Get-Go

12A Registration

The Income Tax Department provides trusts and other non-profit organisations with a one-time registration known as a 12A registration. This registration is being done so that we can avoid having to pay income tax. In most cases, a 12A application is submitted soon after a company’s formation. Clause 8 Businesses, Trusts, and Non-Governmental Organizations (NGOs) that are 12A registered do not have to pay income tax on their surplus funds. Every charitable organisation can take use of the 12A registration option. Hence, Section 12A of the Income Tax Act is a topic that must be understood by all Trusts, NGOs, and other Non-Profit Organizations.

Benefits of 12A Registration

-

The application of the revenue is deemed to constitute the use of the money for religious or philanthropic purposes. For purposes of determining the organization’s taxable income, “income application” means charitable or religious expenditures.

- There won’t be any Income Tax to pay on the money coming in.

- Anybody who qualifies under Section 12A is eligible for tax breaks and other advantages related to saving and investing. But, the reserve fund can’t be more than 15% of the total used for non-profit initiatives.

- Earnings that have accumulated to the point where they qualify as “income application” are excluded from the assessee’s total income.

- Grants in the form of financial support are available to NGOs from both local and foreign sources. These organisations can legally provide money to NGOs that have registered under this provision.

- Registration under this Section12A shall be considered a one-time registration. The registration will remain active till the day it is cancelled.

- Periodic renewal of the registration is not required. So, NGOs can take use of their registered benefits whenever they are needed.

Eligibility for 12A Registration

- The organisation must have a charitable purpose, as defined by the Income Tax Act, in order to be eligible for registration under Section 12A. The impoverished, those in need of education or medical care, and the environment are all candidates for charitable use of funds. Charity can be used for anything that serves the public good, including the pursuit of public service goals.

- Assessees will mostly be judged on whether or not their actions are driven by a desire for financial gain. There must be no expectation of financial gain for registration to be denied.

- The assessee is not eligible for the assistance provided by this section if they are engaged in commercial operations. Only if the assessee’s total receipts from all sources are less than 20% of the total receipts from the commercial activity will registration be permitted.

- It should be emphasised that Private or Family Trusts are exempt from 12A Registration. There must to be actual public benefit from the assessee’s actions.

Anyone seeking to register under Section 12A must do so by filing Form 10A. Applying for a Section 12A registration and submitting a Form 10A have both been streamlined into entirely digital processes. Filing documents electronically requires the use of a digital signature. The trust’s creator or author’s digital signature is required for a Section 12A application. For purposes of Section 12A registration, a Form 10A application can be filed by a religious or philanthropic organisation. Online submission of the application is required. You need to send your application and supporting paperwork to the Income Tax Commissioner.

Documents Required for 12A Registration

- A self-certified copy of the instrument which was used to create the trust or establish the institution shall be submitted.

- The institution or trust may have been created otherwise than by way of drafting and registering an instrument. In such cases, a self-certified copy of the document evidencing the creation of the trust, or establishment of the institution should be submitted to the Income Tax Department.

- It is necessary to submit a self-certified copy of the registration, which was made with the applicable body. The applicable body may be the Registrar of Companies, the Registrar of Firms and Societies or Registrar of Public Trusts.

- A self-certified copy of the documents which provide evidence for adoption or modification of the objectives of the entity shall be submitted.

- Annual financial statements for three preceding financial years

- Note on the activities conducted by the entity

- In certain cases, the Income Tax department may cancel the registration granted under this section. After rectifying the default, the assessee is allowed to make a subsequent application. In such cases, it is necessary to submit a self-certified copy of the existing order granting registration.

- The assessee may have previously applied for registration under this section. The application may have been rejected. In such cases, a self-certified copy of the order of rejection should be attached with the application.

Procedure for Obtaining 12A Registration

- The application must be submitted by the assessee online in the specified format. The Commissioner may ask for more information or supporting materials after an application has been submitted. If the Internal Revenue Service has to be convinced that the trust’s actions are legitimate, the Commissioner may make such a request.

- The application could perhaps impress the Commissioner. Once an assessee meets the requirements for section registration, the Commissioner will issue a formal order stating as much. The assessee is given a copy of the written order. The assessee is entitled to the benefit of registering under this provision upon receipt of the order.

- There is a chance that the commissioner will reject the application. The Commissioner retains the option to decline the application in such circumstances. A written explanation of the rejection’s basis should be provided to the assessee.

If you require this service, you are requested to contact our compliance manager 08943620159 or by email at info@techmincsc.in.

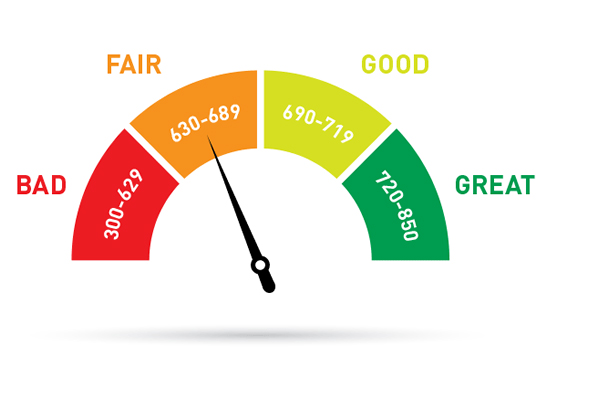

Check CIBIL Score Now

CIBIL Score is a three-digit numeric summary of your credit history. The score is derived using the credit history found in the CIBIL Report (also known as CIR i.e Credit Information Report).

A CIR is an individual’s credit payment history across loan types and credit institutions over a period of time

Copyright © 2024 TECHMIN CONSULTING | Powered by TECHMIN CONSULTING