Do Your Best From The Get-Go

80G Registration

If you have made gifts to a charity trust or a Section 8 firm or organisation that is registered to grant you exemptions from taxes, you may be eligible to get a tax exemption certificate with a value of up to 100 percent. For e.g. To qualify for the section 80G tax deduction, the charity or trust must be registered as a section 12 A organisation. But, there is a limit to how much can be deducted. If your total donations surpass 10% of your gross income, you will not receive a tax deduction for the excess. In 1967–68, Congress codified the 80G certificate as a significant tax deduction.

Who can avail tax savings under 80G?

- Donors can get a tax break under section 80 G if they give to qualified organisations.

- Only contributions to the organisations and trusts on the approved list are tax deductible under section 80G.

Who cannot avail tax savings under section 80G?

- Donations to foreign trusts are not eligible for section 80G tax benefits.

- You cannot take advantage of or claim a deduction for contributions made to one or more political parties. Brochures, flyers, and booklets cannot be deducted either because they are printed or published.

- Section 80G of the Internal Revenue Code exempts nonresident aliens from paying taxes on donations they make to certain types of nonprofit organisations.

- In accordance with section 80G of the Internal Revenue Code, employees are eligible for a tax deduction for salary-based donations that include the employer’s name on the accompanying receipt.

Percentage of Deduction under Section 80G

- There is no cap on the amount of money that can be deducted as a result of contributions to the Prime Minister’s Relief Fund.

- Contributions to the “Indira Gandhi memorial trust” are fully deductible at the rate of 50%.

- Institutions that actively support and encourage family planning are entitled for a full exemption under section 80G.

- Generally, u/s 80G allows for a 50% deduction for contributions to any charity trust that qualifies.

80G Registration – Compliance Requirements

- Only organisations meeting these criteria—public charities, registered societies, accredited universities, and government-funded organizations—are eligible to apply.

- The certificate can only be issued to a trust or organisation that is properly registered under the Societies Registration Act, 1860, Section 25 of the Companies Act, or any other applicable Acts.

- Certificate applicants must not be associated with any group that discriminates on the basis of religion or caste.

- The designated trust or organisation must use the donations only for their intended philanthropic objectives.

- There shouldn’t be any non-exempt funds held by the registered trust/institution.

- In order to keep the funds donated to one cause distinct from the funds saved for another endeavour, organisations should keep them in a different account.

- Before applying for the certification, the applicant must have kept up with the necessary yearly returns, accounting, and bookkeeping.

- A certificate holder’s ability to claim tax breaks depends on how diligently they maintain their certifications and make sure they are renewed on time.

Process of Obtaining 80G Registration

The Commissioner of Income Tax shall handle applications for registration under this provision once they have been submitted on Form 10G. The following materials must be included with the application:

- A Certificate of Registration, Memorandum of Association, or Trust Deed with a No Objection Certificate from the property owner of the Registered Office’s physical location.

- A photocopy of the institution’s Pan card.

- A recent utility or water bill, or a copy of your property tax statement, is required.

- Documentation of the nonprofit’s commitment to social justice during the course of its first three years in operation.

- A financial statement and balance sheet covering the inception and preceding three years

- Address and PAN numbers of all donors are listed.

- Contact information for the board of directors

- A copy of the registration issued under Section 12A, a copy of the notice given under Section 10(23), or a copy of Section 10 (23C)

Issue of Certificate

After reviewing the application, the Commissioner may issue a written order registering the trust/institution under Section 80G of the Income-tax Act. Moreover, the Commissioner has the authority to request additional information from the applicant or to deny the application altogether. The trust will be registered for a term of one to three years.

If you require this service, you are requested to contact our compliance manager 08943620159 or by email at info@techmincsc.in.

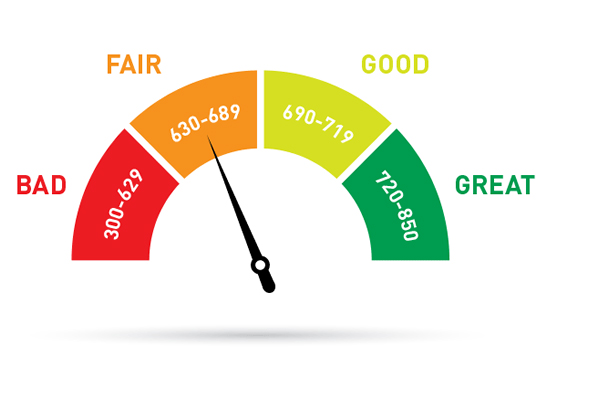

Check CIBIL Score Now

CIBIL Score is a three-digit numeric summary of your credit history. The score is derived using the credit history found in the CIBIL Report (also known as CIR i.e Credit Information Report).

A CIR is an individual’s credit payment history across loan types and credit institutions over a period of time

Copyright © 2024 TECHMIN CONSULTING | Powered by TECHMIN CONSULTING